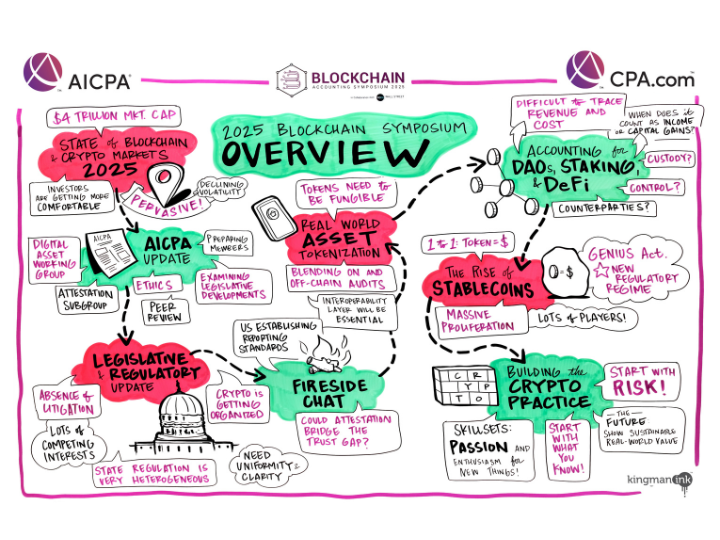

Expert guidance and tools to help you grow your practice CPA.com Resources Use the filters to select complimentary content that will help you grow your expertise in the practice area and services that matter most to you. LOADING... No Audit & Assurance-Digital CPA-Practice management-Strategy-Talent-TechnologyClient Advisory Services-Bill pay-Digital CPA-Financial planning & analysis-Financing advisory-Human resources advisory-Practice management-Spend & expense management-SSARS-Strategy-Talent-TechnologyFirm Management-Branding-Digital CPA-Human capital management-Strategy-Talent-Technology-Web domainsInnovation-Artificial intelligence-Blockchain & digital assets-Digital CPA-ESG-Profession insights-Technology trendsTax-Digital CPA-Personal financial planning-Practice management-Sales & use tax-Strategy-Talent-Tax Research AI-TechnologyCPEContent Type-Blog articles-Conferences-eBooks-Guides-Infographics-Live news broadcasts-Newsletters-Podcasts-Product demos-Reports-Success stories-Toolkits-Videos-Webinars--Upcoming webinars--On-demand webinars-Whitepapers Content Type-Blog articles-Conferences-eBooks-Guides-Infographics-Live news broadcasts-Newsletters-Podcasts-Product demos-Reports-Success stories-Toolkits-Videos-Webinars--Upcoming webinars--On-demand webinars-Whitepapers Apply 1 hour How CAS Firms Are Unlocking New Potential with Agentic... Client advisory services (CAS) practices are evolving fast—and AI is leading the charge. From streamlining vendor onboarding to real-time... Read more Client Advisory Services, Webinars, On-demand webinars 1 hour Automate, scale, advise: The new AI-powered sales tax... Expanding into sales and use tax advisory doesn’t have to overextend your team or require deep tax specialization. Join CPA.com, Vertex, and... Read more Tax, Sales & use tax, Technology, Webinars, On-demand webinars 5 minute read Building SQMS No. 1 into your firm For many CPA firms, implementing SQMS No. 1 begins with building the foundation: documenting quality objectives, identifying quality risks... Read more Audit & Assurance, Technology, Blog articles 1 hour Navigating the Next Wave of AI in Tax Research Artificial intelligence is evolving from an emerging trend to a critical driver of change in tax research. As adoption accelerates, new... Read more Tax, Tax Research AI, Webinars, On-demand webinars 1 hour Positioning CAS for Growth: How to Market, Message, and... Many firms struggle to explain the value of CAS — both to clients and internally. Without clear positioning and a strong message, even the... Read more Client Advisory Services, Webinars, On-demand webinars 1 hour Reimagining Tax Season with AI It’s that time of year again. Tax season is ramping up, and accountants everywhere are preparing for the long days (and nights) ahead. But... Read more Tax Research AI, Webinars, On-demand webinars Why is requiring a CAS tech stack so important? Richard Corn, CPA, Director of Product Management at BILL discusses the importance of adopting a standardized tech stack across clients for... Read more Client Advisory Services, Bill pay, Videos Quick tips to ensure your firm is using technology... Richard Corn, CPA, Director of Product Management at BILL offers his advice on keeping your tech stack working properly for you, your team... Read more Client Advisory Services, Bill pay, Videos 4 minute read How growing digital asset adoption is reshaping... Top themes from the AICPA and CPA.com Blockchain in Accountancy Symposium Watch a discussion on key takeaways from the Blockchain in... Read more Innovation, Blockchain & digital assets, Blog articles 5 minute read AI adoption in accounting is rising, but trust lags AI isn’t coming to accounting, it’s already here. From auto-classifying transactions to enhancing audit procedures, the technology is... Read more Innovation, Artificial intelligence, Digital CPA, Blog articles How Agentic AI Is Transforming CAS Workflows (and What... Client advisory services (CAS) are at a pivotal moment. As client expectations rise and staffing constraints persist, accounting firms are... Read more Client Advisory Services, Bill pay, Spend & expense management, Technology, Whitepapers 1 hour Monitoring & Remediation: Building a Practical, Risk... As firms continue to refine their risk assessment, monitoring, and remediation processes, expectations around how monitoring is designed and... Read more Audit & Assurance, Webinars, On-demand webinars Pagination First page « First Previous page ‹ Previous Page 1 Page 2 Page 3 Current page 4 Page 5 Page 6 Page 7 Page 8 Page 9 … Next page Next › Last page Last »

LOADING...

LOADING...