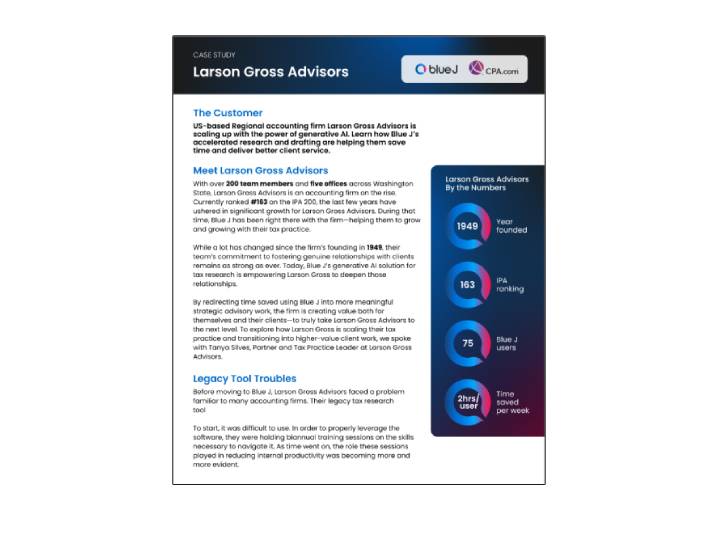

Expert guidance and tools to help you grow your practice CPA.com Resources Use the filters to select complimentary content that will help you grow your expertise in the practice area and services that matter most to you. LOADING... No Audit & Assurance-Digital CPA-Practice management-Strategy-Talent-TechnologyClient Advisory Services-Bill pay-Digital CPA-Financial planning & analysis-Financing advisory-Human resources advisory-Practice management-Spend & expense management-Strategy-Talent-TechnologyFirm Management-Branding-Digital CPA-Human capital management-Strategy-Talent-Technology-Web domainsInnovation-Artificial intelligence-Blockchain & digital assets-Digital CPA-ESG-Profession insights-Technology trendsTax-Digital CPA-Personal financial planning-Practice management-Sales & use tax-Strategy-Talent-Tax Research AI-TechnologyCPEContent Type-Blog articles-Conferences-eBooks-Guides-Infographics-Live news broadcasts-Podcasts-Product demos-Reports-Success stories-Toolkits-Videos-Webinars--Upcoming webinars--On-demand webinars-Whitepapers Content Type-Blog articles-Conferences-eBooks-Guides-Infographics-Live news broadcasts-Podcasts-Product demos-Reports-Success stories-Toolkits-Videos-Webinars--Upcoming webinars--On-demand webinars-Whitepapers Apply 2025 AI in Accounting Report What was once seen as a technological advancement has quickly become a strategic imperative. Explore the latest report, which serves as a... Read more Innovation, Artificial intelligence, Reports Procure, pay, predict: Power CAS with tech innovations Your ecommerce client is confronted with sudden supplier price spikes, looming invoice backlogs and persistent cash-flow uncertainty. They... Read more Client Advisory Services, Technology, Blog articles 3 minutes How AI can boost your firm’s recruitment efforts On any given week, how much of your firm’s time and resources are spent on recruitment? Probably way more than you’d like, especially when... Read more Human resources advisory, Firm Management, Blog articles 2 minutes Who DCPA is for and why it’s grown year after year DCPA has evolved into a must-attend event for forward-thinking professionals in the accounting profession. In this video, Kimberly Ellison... Read more Innovation, Digital CPA, Videos 30 seconds CPA Business Funding Portal Testimonial: Tiffany... Tiffany Jackson, Owner of TW Tax & Credit Services, shares why she loves the CPA Business Funding Portal and how it helps speed up the... Read more Client Advisory Services, Videos CPA.com and BILL growth & technology survey High-tech. High-yield. High-growth. The accounting profession is evolving faster than ever. Firms with a forward-thinking vision are seizing... Read more Client Advisory Services, Bill pay, Technology, Reports AI Symposium Takeaways Read more Innovation, Artificial intelligence, Technology trends, Videos 3 minutes Drive real change in your audit firm Every audit firm is feeling the pressure to modernize—faster delivery, better tools and smarter processes. But audit transformation isn’t... Read more Audit & Assurance, Digital CPA, Practice management, Blog articles 5 minute read Shaping the future: 6 Takeaways from the AICPA and CPA... At the 2nd annual 2025 AICPA and CPA.com AI in Accounting and Finance Symposium, accounting and finance leaders, technology solution... Read more Innovation, Artificial intelligence, Profession insights, Blog articles 4 minute read How small firms are making big-firm tech moves The pace of new technology hitting the market is relentless—and for many accounting firms, especially smaller ones without dedicated IT... Read more Firm Management, Technology, Web domains, Blog articles 5 minute read Cracking the CAS growth code The client advisory services (CAS) practice area continues to present one of the most compelling growth opportunities for accounting firms... Read more Client Advisory Services, Practice management, Strategy, Blog articles Larson Gross Advisors Curious how accounting firms are scaling smarter with generative AI? Learn how Larson Gross Advisors transformed their tax research with... Read more Artificial intelligence, Tax Research AI, Success stories Pagination First page « First Previous page ‹ Previous Page 1 Current page 2 Page 3 Page 4 Page 5 Page 6 Page 7 Page 8 Page 9 … Next page Next › Last page Last »

LOADING...

LOADING...